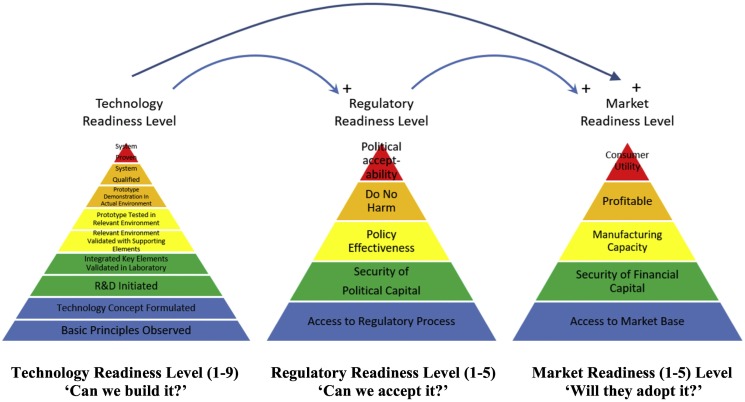

CSR Advisory and Audits focus on planning, implementing, and evaluating Corporate Social Responsibility initiatives. This includes guiding companies on effective CSR strategies and conducting audits to ensure activities comply with legal requirements and create meaningful social impact.

12 May 2026

Corporate Social Responsibility in India is a legal requirement for thousands of companies. Section 135 of the Companies Act, along with the Companies CSR Rules, mandates that eligible companies spend at least two percent of their average net profits from the preceding three years on CSR activities. This has created a predictable flow of funds into social development. But here is the question that separates ordinary companies from exceptional ones. Is your CSR just about spending the money, or is it about creating lasting value for both the community and your business? Strategic CSR moves beyond writing cheques to trusted non profits. It aligns social impact with business expertise, employee passion, and geographic presence. It turns a compliance obligation into a source of brand strength, employee pride, and genuine community goodwill. This article explores how Indian companies can make that shift. From passive philanthropy to active, strategic citizenship. The compliance trap that holds companies backEvery year, as the new financial year begins, CSR committees across India gather to address the same question. How do we spend our mandated two percent? The pressure is real. Funds must be allocated. Projects must be identified. Implementing partners must be selected. Reports must be filed. The cycle is annual, predictable, and often rushed. The result is a familiar pattern. A company identifies a few broad sectors. Education, healthcare, skill development, environmental conservation. They invite proposals from non profits. They select a handful of projects based on proposal quality, personal connections, or what other companies are doing. They disburse funds. They collect some photographs and testimonials. They file their annual report. They start again next year. This approach ensures compliance. It meets the letter of the law. But it fails to meet the spirit of the law. The Companies Act was not designed to create a cheque writing exercise. It was designed to harness corporate resources for genuine social development. Unfortunately, many companies remain trapped in a compliance mindset. They treat CSR as a tax on profitability rather than an opportunity for meaningful engagement. The cost of this compliance trap is not just missed opportunity. It is wasted resources, shallow impact, and employee cynicism. When employees see their company treating CSR as a bureaucratic requirement rather than a genuine commitment, they disengage. When communities sense that a company is only present because the law requires it, they do not trust. And when the impact is shallow, the co :mpany has nothing to show for its investment beyond a filed report. Strategic CSR offers a way out of this trap What strategic CSR truly means: Strategic CSR is not a single definition. It is a different way of thinking about the relationship between a company and society. At its simplest level, strategic CSR means aligning a company's social initiatives with its core business expertise, its operational footprint, and its long term interests. It moves the conversation from what should we fund to what can we uniquely contribute. It recognises that a company brings more to the table than money. It brings people, skills, technology, networks, distribution channels, and deep local knowledge. A pharmaceutical company practicing strategic CSR does not simply fund a general health camp. It might focus on improving access to essential medicines, strengthening vaccine cold chains, or supporting research on neglected tropical diseases. These initiatives draw on what the company knows best. They create impact that a non pharmaceutical company could not easily replicate. And they reinforce the company's identity as a health focused organisation. A technology company practicing strategic CSR does not simply donate old computers to a school. It might develop digital literacy curricula, train teachers on technology integration, or build software tools for government schools. These initiatives use the company's core capabilities. They create impact that lasts beyond the donation. And they build a pipeline of future talent who have grown up using the company's products. A bank practicing strategic CSR does not simply fund a livelihood program. It might offer financial literacy workshops, provide mentorship to women entrepreneurs, or develop accessible banking products for rural customers. These initiatives connect directly to the bank's core business. They build trust with future customers. And they demonstrate that the bank understands the real financial needs of ordinary people. This is the essence of strategic CSR. Using your company's distinctive strengths to solve problems that your company is uniquely positioned to solve. The Indian advantage. Local knowledge and distribution networksIndia offers a particularly fertile ground for strategic CSR. The reasons are rooted in the country's economic and social structure. First, many Indian companies have deep roots in specific regions. A company may have operated in a particular district for decades. It knows the local language, the local power structures, the local needs, and the local trusted institutions. This knowledge is invaluable for designing effective social programs. An outsider would take years to develop the same understanding. A local company starts with it. Second, Indian companies often have extensive distribution networks. A fast moving consumer goods company reaches millions of retail outlets across the country. A logistics company has fleets, warehouses, and route networks. A telecommunications company has towers and retail presence in even the most remote areas. These networks can be leveraged for social good. Health supplies can ride on logistics trucks. Educational content can be delivered through telecom infrastructure. The same networks that move products can also move social value. Third, Indian employees care deeply about social contribution. Surveys consistently show that Indian professionals, particularly younger ones, want to work for companies that make a positive difference. Strategic CSR gives employees a reason to feel proud. It becomes a tool for talent attraction and retention. In a competitive labour market, that is a significant advantage. Fourth, India's development challenges are vast and varied. There is no shortage of meaningful work to be done. A company can choose a focus area that genuinely aligns with its expertise and know that it is addressing a real need. The opportunity for alignment is unusually rich. These advantages are available to any Indian company that chooses to use them. But they require intention. They require strategy. They do not happen by accident. A practical framework for strategic CSRFor companies ready to move beyond compliance and into strategy, here is a practical framework. It consists of five sequential steps. ➢ Inventory your core competencies.Begin by asking a simple question. What does our company do better than most other companies? Be specific. Do not say we are good at management. Say we are excellent at cold chain logistics. We have world class expertise in water purification. Our sales force is the best trained in the industry. Write down three to five genuine, demonstrable strengths. These will become the foundation of your CSR strategy. ➢ Map competencies to social needs.For each core competency, ask which social or environmental problem your company is uniquely positioned to address. A cold chain logistics company might focus on reducing vaccine waste in remote areas. A water purification company might focus on providing clean drinking water in fluoride affected districts. A well trained sales force might be deployed to spread awareness about nutrition or sanitation. The overlap between your strengths and society's needs is your strategic sweet spot. ➢ Choose a geographic focus.Many Indian companies spread their CSR budget thinly across many districts or even many states. This is almost always a mistake. Deep impact requires concentrated resources. Choose one, two, or three districts where your company already has a significant presence. Your employees live there. Your suppliers operate there. Your customers are there. You understand the local context. You can monitor projects effectively. You can build lasting relationships. Go deep, not wide. ➢ Design projects that leverage your assets.Do not simply write a cheque to an implementing partner. Ask how your company's people, technology, facilities, or networks can add value. Can your engineers volunteer their time? Can your underutilised office space host a training program? Can your distribution network deliver educational materials? The cheque is important, but the engagement is transformative. Design projects that could not succeed without your company's unique contribution. ➢ Measure outcomes, not just outputs.Outputs are easy to count. Number of workshops conducted. Number of people trained. Number of trees planted. Outcomes are harder to measure but much more meaningful. Improvement in learning outcomes. Increase in household income. Reduction in disease incidence. Commit to measuring outcomes from the beginning. Build a simple, credible measurement framework. Use it to learn and improve. Share the results transparently. This framework is not theoretical. It has been applied successfully by companies of all sizes across India. The specific details vary, but the underlying logic remains consistent. Align. Focus. Leverage. Measure. The employee engagement dividendOne of the most powerful benefits of strategic CSR is its effect on employee engagement. When employees see their company using its core strengths to solve real problems, they feel a sense of purpose that transcends their daily tasks. Strategic CSR creates opportunities for employee volunteering that are genuinely meaningful. An engineer from a water company can test water quality in a rural school. A banker can teach financial literacy to women entrepreneurs. A logistics professional can help a non profit optimise its supply chain. These are not token activities. They use employees' professional skills. They respect their expertise. They create experiences that employees remember and value. This matters for retention. In a competitive labour market, employees have choices. They increasingly choose employers who share their values and offer a sense of purpose. Strategic CSR communicates those values more credibly than any mission statement. It turns the workplace into a source of pride. This also matters for recruitment. Young professionals, in particular, want to know that their work contributes to something larger than shareholder returns. A company with a clear, credible, strategic CSR program stands out. It attracts talent that might otherwise go elsewhere. The brand and stakeholder trust advantageStrategic CSR also builds brand value. But it does so quietly and authentically, not through loud self promotion. When a company consistently supports a cause that aligns with its expertise, stakeholders notice. Customers perceive the company as genuine rather than performative. Investors see reduced risk and enhanced reputation. Regulators view the company as a responsible partner rather than a potential violator. Local communities welcome the company as a contributor rather than resisting it as an extractor. These benefits accumulate over time. Trust is built slowly and lost quickly. Strategic CSR is a long term investment in trust. It signals that the company is not just present to profit, but to contribute. There is also a defensive benefit. Companies with strong CSR reputations face less criticism from activists, less scrutiny from regulators, and less resistance from local communities. Strategic CSR does not immunise a company against legitimate criticism, but it builds a foundation of goodwill that helps the company weather difficult moments. How strategic CSR simplifies compliance and auditHere is a practical benefit that compliance officers will appreciate. Strategic CSR actually makes compliance and auditing easier, not harder. When CSR is ad hoc and reactive, every audit is a struggle. The auditor asks why a particular project was chosen. There is no coherent answer. The auditor asks how impact is measured. There is no consistent framework. The auditor asks whether funds were used efficiently. There is no benchmark for comparison. Every answer is defensive. Every finding is a surprise. When CSR is strategic, every decision is grounded in a clear rationale. This project was chosen because it aligns with our core competency in logistics. This geographic area was chosen because we already operate there and understand the local context. This implementing partner was selected because they have a proven track record in our focus area. The answers are clear, consistent, and defensible. Strategic CSR also simplifies reporting. Instead of compiling a random collection of project updates, the company tells a coherent story. Here is our focus area. Here is our theory of change. Here are the outcomes we have achieved. Here is how we are learning and improving. That kind of report satisfies both legal requirements and stakeholder expectations. The long term orientation. Patience as a strategic virtueStrategic CSR requires patience. Social change does not happen on quarterly cycles. A child's educational trajectory unfolds over years. A community's health outcomes improve slowly but measurably. A degraded ecosystem recovers over decades. The best strategic CSR programs are designed for the long term. They commit to a cause, a geography, and a set of partners for years, not months. They build relationships based on trust and mutual respect. They learn what works and what does not work. They adjust their approach based on evidence. They do not abandon good work just because a new financial year has begun. This long term orientation is a genuine competitive advantage because most companies lack patience. They chase new causes every year based on what is fashionable. They switch geographies based on convenience. They change partners when relationships become slightly difficult. A company that stays the course will eventually achieve impact that scattered competitors cannot match. Common mistakes to avoidAs companies shift toward strategic CSR, several common mistakes deserve attention. ✗ Choosing a focus area that is too broad. Education, for example, is not a focus area. It is an entire sector. A strategic focus might be improving foundational literacy in government primary schools in two specific districts. That is narrow enough to be meaningful. ✗ Expecting quick results. Strategic CSR is a long term commitment. Companies that expect to see transformation within one year will be disappointed. A three to five year horizon is more realistic. ✗ Treating strategic CSR as a replacement for responsible business practices. A company cannot pollute freely and then fund environmental projects as compensation. Strategic CSR is meant to address social and environmental issues beyond the company's legal obligations. It is not a licence to ignore those obligations elsewhere. ✗ Failing to communicate strategically. Many companies do excellent CSR work but never tell the story. Others tell the story poorly, focusing on their own generosity rather than the community's progress. The right approach is transparent, humble, and focused on outcomes. ✗ Doing strategic CSR alone. The most complex social problems require collaboration. Companies should partner with non profits, government agencies, other companies, and community based organisations. No single actor has all the answers. The true measure of strategic CSRHow does a company know when it has truly embraced strategic CSR? The answer lies in a few key indicators. 1. The CSR strategy is discussed at the board level, not just the department level. Directors understand and support the logic. 2. The CSR portfolio has a clear thematic coherence. An outside observer could look at the portfolio and identify the company's focus area without being told. 3. Employees can articulate the company's CSR strategy in a sentence or two. It is not a secret known only to the CSR department. 4. The company has stayed committed to the same focus area and geography for at least three years. There is evidence of learning and improvement, but not of abandonment. 5. The company measures outcomes, not just outputs. It can demonstrate change in the lives of the communities it serves. 6.The CSR program generates tangible business benefits. Employee engagement has improved. Brand perception has strengthened. Local relationships have deepened. These benefits are not the goal of strategic CSR, but they are reliable indicators that the strategy is working. When these indicators are present, a company has successfully moved beyond the cheque. It has turned compliance into competitive advantage. It has discovered that doing good, done intelligently and strategically, is also good business. ...Read more

12 May 2026

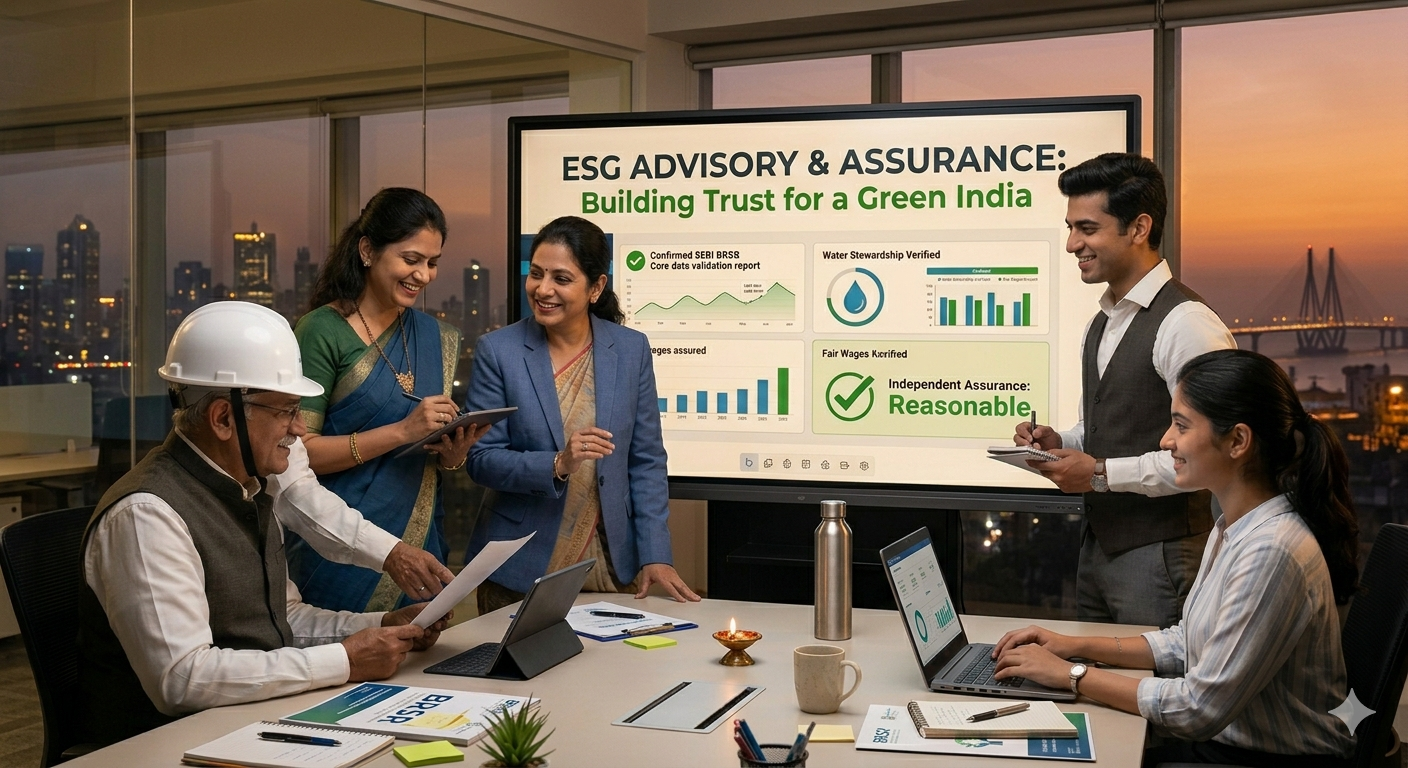

In the mahogany-paneled boardrooms of Mumbai and the high-tech hubs of Bengaluru, a new language is being spoken. It is not the language of quarterly profits or market share alone, but a more complex dialect of "materiality," "scope emissions," and "social equity." This is the era of ESG (Environmental, Social, and Governance), and for the Indian professional, it represents the most significant shift in corporate accountability since the introduction of independent audits. At its heart, ESG Advisory and Assurance is about one thing: trust. It is the process of proving that a company's promises to the planet and its people are backed by data, not just marketing. In India, where the gap between corporate ambition and grassroots reality can be wide, the role of the advisor and the assurer is to bridge that divide with integrity. To understand this landscape in 2026, we must look past the spreadsheets and see the human stories of transformation that are redefining Indian business. The Advisory Horizon: Crafting a Strategy with a SoulESG Advisory is often mistaken for a compliance exercise, especially as the Securities and Exchange Board of India (SEBI) has made Business Responsibility and Sustainability Reporting (BRSR) mandatory for the top 1,000 listed entities. However, the most successful Indian firms view advisory as a strategic compass. 1. Beyond the "Tick-Box" CultureFor many years, corporate responsibility in India was synonymous with CSR (Corporate Social Responsibility)—the 2% of profits spent on philanthropy. Advisory in 2026 has moved far beyond this. It is about integrating sustainability into the very DNA of the business model. When an advisor walks into a traditional textile mill in Tiruppur, they aren't just looking for solar panels. They are looking at the health and safety of the workers, the transparency of the chemical supply chain, and the long-term viability of the water sources. The humanized narrative here is the transition of a business owner from a "boss" to a "steward." Advisory helps these leaders understand that protecting the river they draw water from is not a cost—it is an investment in their own survival. 2.The Great Decarbonization RoadmapIndia’s commitment to Net Zero by 2070 has put immense pressure on heavy industries like steel and cement. ESG advisors are the architects of this transition. They help firms navigate the "Climate Finance Taxonomy," a structured system that defines what truly counts as a "green" investment in the Indian economy. The human story in decarbonization is found in the "Just Transition." Advisors work with HR teams to ensure that as a coal-fired plant is decommissioned, the workers are not simply discarded. They are reskilled for the green hydrogen or battery storage roles of the future. This is the "S" (Social) in ESG in action—ensuring that the drive for a cleaner planet does not come at the expense of human dignity. The Assurance Anchor: Building a Fortress of DataIf Advisory is the roadmap, Assurance is the proof that you’ve actually arrived. In a world increasingly skeptical of "greenwashing," third-party verification has become the ultimate currency of credibility. 1.The Death of the "Fluff" ReportUntil recently, many sustainability reports were filled with glossy photos of smiling children and saplings being planted. Assurance has put an end to this. Starting in the 2025-26 fiscal year, SEBI’s BRSR Core framework requires quantifiable, auditable metrics that are as rigorous as financial statements. The process of assurance is deeply technical, but its purpose is human. When an auditor verifies a company’s water-usage data in a drought-prone region like Marathwada, they are providing assurance to the local community that the company isn't depleting their life-source. They are providing assurance to a global investor in London or Singapore that the "risk" of water-related shutdowns has been accurately measured and managed. 2. The Challenge of “Dirty Data”One of the biggest hurdles for Indian firms is data integrity. ESG data is often fragmented across different departments—HR has the diversity stats, Operations has the energy bills, and Procurement has the supplier audits. Assurance professionals act as "data cleaners." They implement systems that track information from the source—like an IoT sensor on a factory chimney—directly to the report. This reduces human error and intentional manipulation. For the professional reader, the takeaway is clear: in 2026, an unverified ESG claim is a liability. It invites regulatory fines, investor flight, and irreparable brand damage. The Financial Ripple Effect: Why Credibility PayThe ultimate reason for the surge in ESG Advisory and Assurance in India is the "Green Premium." Evidence from 2026 shows that Indian firms with high ESG scores and independent assurance demonstrate better financial stability and a lower cost of capital. 1. Lowering the Cost of DebtBanks and NBFCs (Non-Banking Financial Companies) are increasingly offering "Sustainability-Linked Loans" (SLLs). In these arrangements, the interest rate is tied to the company’s ESG performance. If the company meets its carbon reduction or gender diversity targets—verified by an independent assurer—the interest rate drops. This creates a powerful human incentive for change. It turns the CFO into a champion for sustainability because they can directly see the impact on the bottom line. It isn't just about "doing good" anymore. it is about being more profitable through being more responsible. 2. Attracting the Global TitanGlobal institutional investors, managing trillions of dollars, are looking at India as a standout option among emerging markets. However, they are wary of the lack of standardized data. By providing "Reasonable Assurance"—the highest level of audit—Indian firms are effectively speaking the universal language of global finance. Sustainable investing in India is projected to hit $125 billion by 2026. This capital is flowing into sectors like e-mobility, agritech, and waste management. The humanized side of this investment is the creation of a new, green middle class. It is the funding that allows an Indian startup to deploy thousands of electric delivery scooters, providing clean air for the city and a stable income for the drivers. The Governance Pillar: Leading from the TopWhile the "E" and "S" often get the headlines, the "G" (Governance) is the foundation of ESG Advisory. Without strong governance, environmental and social initiatives are destined to fail. 1. Diversity as a Strategic AssetGovernance advisory in India has a strong focus on board diversity. In 2026, this has moved beyond just having one woman on the board to comply with the law. It is about cognitive diversity—bringing in experts in climate science, human rights, and digital ethics to the boardroom. The human story here is the "opening up" of the traditional Indian corporate structure. It is the realization that a board that looks and thinks the same way is a board that is blind to emerging risks. 2. Executive Compensation and AccountabilityA key trend in ESG Advisory is linking executive pay to sustainability targets. When the CEO's bonus is tied to the company’s safety record or its carbon footprint, the entire organization takes note. This shifts the focus from short-term "quarterly-ism" to long-term value creation. It forces a more humanized view of the company’s legacy. Overcoming the Hurdles: The Road to 2030Despite the progress, the path for ESG in India is not without its challenges. The professional community must address: » The Talent Gap: There is a massive shortage of professionals who understand both Indian business realities and global ESG frameworks. Investing in "Green Upskilling" is the most urgent human need in this sector. » SME Integration:While the top 1,000 firms are reporting, the millions of small and medium enterprises (SMEs) that form the backbone of the Indian supply chain are lagging behind. Advisory must find ways to make ESG accessible and affordable for the "Chote Bhai" of Indian industry. » Data Standardisation: 73% of investors still find ESG ratings inconsistent. The move toward SEBI-registered rating providers is a step in the right direction, but we need more harmony between Indian and global standards. Conclusion: The New Social ContractESG Advisory and Assurance are not just technical services. they are the tools we use to write a new social contract for Indian business. They represent a future where a company’s value is measured by its contribution to the world, not just its extraction from it. As professionals, our role is to ensure that this transition is rooted in reality. We must be the ones who ask the hard questions, who demand the verified data, and who never lose sight of the human being at the other end of the supply chain. In the bustling markets and quiet villages of India, the green shift is happening. By bringing credibility to this shift, we are building an India that is not just a global economic powerhouse, but a global moral leader. The "Green Budget" of 2026-27 and the rise of the Carbon Credit Trading Scheme are just the beginning. The real work happens every day, in the diligent collection of data and the courageous setting of targets. Let us build a corporate India where transparency is the light, and trust is the energy that moves us forward. ...Read more

12 May 2026

In today’s rapidly evolving business environment, companies are no longer evaluated solely on the basis of profit and market performance. Consumers, investors, governments, and communities increasingly expect businesses to contribute positively to society while operating in an ethical and transparent manner. This growing expectation has made Corporate Social Responsibility, commonly known as CSR, an essential part of modern business strategy rather than a voluntary add on. Corporate Social Responsibility refers to the efforts made by businesses to contribute toward social, environmental, and economic well being beyond their primary commercial activities. CSR initiatives may focus on education, healthcare, environmental sustainability, rural development, women empowerment, skill development, sanitation, community welfare, and many other areas that create positive societal impact. However, simply launching CSR activities is not enough. Businesses today are expected to ensure that their CSR programs are meaningful, transparent, legally compliant, and capable of generating measurable impact. This is where CSR Advisory and Audits become increasingly important. CSR Advisory helps organisations design, implement, and manage effective social responsibility strategies aligned with both business values and community needs. CSR Audits, on the other hand, evaluate whether these initiatives are being carried out responsibly, efficiently, and in compliance with regulatory frameworks. Together, CSR Advisory and Audits help companies move beyond symbolic social initiatives toward creating long term, accountable, and sustainable impact. Understanding the Importance of CSR in Modern BusinessThe relationship between businesses and society has changed significantly over the past few decades. Earlier, companies were primarily expected to generate profits, create employment, and contribute to economic growth. While these responsibilities remain important, businesses are now also expected to address broader social and environmental challenges. This shift has been driven by multiple factors. Growing awareness regarding climate change, rising social inequality, environmental degradation, labour rights concerns, and ethical business practices has increased pressure on organisations to operate responsibly. Consumers today often prefer brands that demonstrate social consciousness and environmental commitment. Investors are also paying greater attention to Environmental, Social, and Governance standards when evaluating companies. Businesses that ignore social responsibility may face reputational risks, reduced public trust, and increasing regulatory scrutiny. In India, CSR has become especially significant because of the country’s diverse social and developmental challenges. Issues such as poverty, educational inequality, healthcare accessibility, rural infrastructure, unemployment, and environmental stress continue to affect millions of people across different regions. Corporate participation in social development therefore carries enormous potential for creating positive change. India’s CSR Framework and Legal LandscapeIndia became one of the first countries in the world to legally mandate certain companies to spend on CSR activities through the Companies Act, 2013. Under this framework, qualifying companies are required to allocate a percentage of their average net profits toward CSR initiatives. The law also outlines eligible sectors for CSR spending and requires businesses to disclose their CSR activities transparently. This legal structure significantly transformed the corporate approach toward social responsibility in India. CSR shifted from being viewed primarily as philanthropy to becoming a structured and strategic component of corporate governance. Cities such as Mumbai, Bengaluru, Delhi, Hyderabad, and Kolkata have become major centres for CSR planning, sustainability consulting, social impact partnerships, and compliance management. As CSR regulations evolved, companies increasingly realised the importance of expert guidance and systematic evaluation. This growing complexity contributed to the rise of specialised CSR Advisory and Audit services. What is CSR Advisory?CSR Advisory involves guiding organisations in planning, implementing, monitoring, and improving their social responsibility initiatives. Many companies genuinely want to contribute positively to society but struggle to identify where to focus, how to allocate resources effectively, or how to measure impact meaningfully. CSR Advisory services help businesses address these challenges by developing structured strategies aligned with organisational goals and community needs. Effective CSR planning requires more than simply donating funds or conducting one time events. Long term impact depends on understanding local realities, identifying genuine social needs, collaborating with stakeholders, and designing sustainable programs. CSR advisors help organisations:✓ Identify priority social sectors✓ Develop strategic CSR frameworks✓ Select suitable implementation partners✓ Ensure legal compliance✓ Measure social impact✓ Improve transparency and reporting✓ Align CSR activities with sustainability goalsThe role of CSR Advisory has become especially important as businesses increasingly recognise that well designed CSR initiatives can strengthen both community relationships and corporate reputation. Moving Beyond Charity Toward Sustainable ImpactOne of the most important changes in modern CSR thinking is the shift from short term charity toward long term sustainable development. Traditional corporate philanthropy often focused on donations, sponsorships, or isolated social activities. While these efforts could provide temporary support, they did not always create lasting impact. Modern CSR strategies focus more on sustainable and measurable outcomes. For example, instead of only donating school supplies, companies may invest in teacher training, digital education infrastructure, rural internet access, or long term scholarship programs. Similarly, environmental CSR projects increasingly focus on renewable energy, water conservation, waste management, afforestation, and climate resilience rather than symbolic environmental campaigns alone. CSR Advisory helps companies design initiatives that create meaningful and sustainable improvements within communities rather than temporary visibility. The Human Side of CSRAt its core, CSR is about people. It reflects the understanding that businesses do not operate in isolation from society. Every company depends on communities, workers, consumers, natural resources, and public infrastructure in some form. CSR initiatives therefore have the potential to improve lives directly. In rural areas, corporate support for education and healthcare can create opportunities for children and families who may otherwise lack access to basic services. Skill development programs can improve employability for young people. Women empowerment initiatives can strengthen economic independence and social participation. Environmental projects can also have deeply human outcomes. Clean water programs, sustainable agriculture initiatives, renewable energy projects, and waste management systems all contribute toward healthier living conditions and stronger community resilience. When designed thoughtfully, CSR programs create value not only for businesses but also for society as a whole. What are CSR Audits?While CSR Advisory focuses on planning and strategy, CSR Audits focus on evaluation, accountability, and compliance. A CSR Audit examines whether a company’s CSR initiatives are being implemented effectively and responsibly. It helps determine whether projects align with legal requirements, financial transparency standards, organisational commitments, and intended social objectives. CSR Audits play an important role in ensuring that CSR activities are not merely symbolic exercises or public relations efforts. An audit may evaluate:✓ Fund allocation and utilisation✓ Compliance with CSR regulations✓ Project implementation processes✓ Documentation and reporting✓ Social impact outcomes✓ Stakeholder engagement✓ Governance and accountability systemsAudits help businesses identify gaps, improve efficiency, strengthen transparency, and ensure that CSR investments generate meaningful results. In recent years, stakeholders have become increasingly concerned about greenwashing and superficial sustainability claims. CSR Audits help build credibility by providing structured evaluation and accountability. Why Transparency and Accountability MatterTransparency has become one of the most important expectations in modern corporate governance. Consumers and investors increasingly want evidence that companies are genuinely committed to responsible practices rather than using CSR only for branding purposes. Clear reporting and regular audits help organisations demonstrate authenticity and accountability. They also improve trust among stakeholders, including employees, investors, regulators, local communities, and implementation partners. For example, if a company claims to support rural education programs, stakeholders increasingly expect measurable evidence such as:✓ Number of schools supported✓ Infrastructure improvements✓ Student outcomes✓ Teacher training initiatives✓ Long term project sustainabilityCSR Audits help organisations evaluate whether intended goals are actually being achieved and whether resources are being used effectively. CSR and Environmental SustainabilityCSR initiatives are increasingly connected to environmental sustainability goals. Many Indian companies are investing in projects related to:✓ Renewable energy✓ Water conservation✓ Waste management✓ Afforestation✓ Plastic reduction✓ Sustainable agriculture✓ Climate adaptationAs environmental concerns continue growing globally, businesses are under increasing pressure to reduce ecological impact and support sustainable development. CSR Advisory services help organisations align social responsibility efforts with broader sustainability frameworks and Environmental, Social, and Governance objectives. This integration is becoming especially important because environmental and social challenges are often interconnected. Water scarcity, pollution, climate change, and resource depletion directly affect public health, livelihoods, and economic stability. The Role of Technology in CSR ManagementTechnology is playing a growing role in improving CSR planning, monitoring, and reporting. Digital platforms now allow organisations to track CSR spending, monitor project implementation, analyse impact data, and maintain compliance documentation more efficiently. Data analytics tools help companies measure outcomes more accurately and identify areas requiring improvement. Geographic Information Systems, mobile applications, and digital dashboards are also being used to monitor field projects in real time, particularly in rural development and environmental sustainability initiatives. Technology improves transparency while making CSR management more structured and measurable. Challenges in CSR ImplementationDespite growing awareness and investment, CSR implementation still faces several challenges. One major issue is the lack of long term planning. Some organisations continue to approach CSR as an annual obligation rather than an integrated sustainability strategy. Another challenge involves identifying genuine community needs. Without proper research and stakeholder engagement, CSR projects may fail to create meaningful impact. Monitoring and impact measurement also remain difficult for many organisations. Social progress is often complex and cannot always be measured through short term numerical indicators alone. Additionally, smaller organisations sometimes struggle with compliance requirements, reporting standards, and documentation processes. In certain cases, CSR initiatives may also become overly focused on visibility rather than sustainability. CSR Advisory and Audits help address these challenges by providing professional guidance, evaluation systems, and accountability frameworks. Building Responsible Businesses for the FutureThe future of business will increasingly depend on trust, accountability, and sustainability.Companies are no longer judged only by financial performance but also by how responsibly they contribute to society and the environment. CSR Advisory and Audits support this transformation by helping businesses develop more thoughtful, transparent, and impactful social responsibility strategies. In India, where businesses have the opportunity to contribute toward large scale social development, responsible CSR practices can play a meaningful role in addressing educational inequality, healthcare access, environmental sustainability, skill development, and community welfare. Corporate responsibility is gradually evolving from being a compliance requirement into a broader philosophy of ethical and sustainable business leadership. ConclusionCSR Advisory and Audits have become essential components of responsible corporate governance in the modern business environment. They help organisations move beyond symbolic social initiatives toward creating measurable, transparent, and sustainable impact. Through strategic planning, effective implementation, accountability systems, and continuous evaluation, businesses can ensure that their CSR efforts genuinely benefit communities while aligning with long term sustainability goals. For India, the importance of effective CSR is especially significant. With growing economic influence comes greater responsibility to contribute toward inclusive and sustainable development. Well designed CSR programs can support education, healthcare, environmental protection, women empowerment, rural development, and many other critical social priorities. At the same time, audits and accountability mechanisms help ensure that these efforts remain transparent, ethical, and impactful. Ultimately, CSR is not only about compliance or reputation management. It reflects a deeper understanding that businesses and society are interconnected. The most successful companies of the future will not simply be those that generate profits, but those that create value responsibly while contributing positively to the world around them. ...Read more

26 Mar 2026

The night the ledger learned the word “society” It is late March. The office lights are still on. Coffee has stopped being a beverage and started behaving like a policy. A finance head, a CSR manager, and an anxious CFO are staring at the same figure—one that feels less like a number and more like a deadline. “Have we spent the CSR amount?” A pause follows. Then the quieter sentence that usually comes next, because it carries the weight of law. “If we don’t, we’ll have to disclose reasons.” “And if we still don’t?” “There are troubles ahead.” That single exchange captures the full arc of India’s mandated Corporate Social Responsibility (CSR) story: it began as a disclosure-first experiment and evolved into a tighter compliance-and-accountability regime—deadlines, designated accounts for unspent money, stronger reporting, and the expectation that impact can be measured, not merely described. Before the law: when CSR meant “philanthropy with a founder’s signature” Long before CSR became statutory, corporate giving in India often looked like a family tradition. A hospital near a plant. A school in a hometown. Scholarships for a district where the brand was born. Some of it was heartfelt, some reputational, but much of it lived outside a national framework. The absence of common standards created a predictable twin outcome: genuine work often stayed invisible beyond local memory, and superficial work could hide behind photo opportunities. Then came the turning point: Section 135 of the Companies Act, 2013, which made India one of the first countries to legally mandate CSR spending at scale. The legal core, in plain language: what the law actually asks companies to do India’s CSR design is deceptively simple to state and complicated to execute. If a company is sufficiently large—measured by financial thresholds—it falls under CSR obligations. The headline norm is equally blunt: eligible companies should spend at least 2% of the average net profits of the previous three years on CSR activities. The law nudges companies toward proximity and legitimacy by saying they should give preference to local areas around their operations. And it limits what qualifies as CSR by linking it to Schedule VII, a defined menu of themes—poverty, health, education, sanitation, environment, and allied social priorities. This became the architecture: thresholds, the 2% norm, a defined theme list, and board-level disclosure. A policy that refused to stay still: the decade-plus timeline of tightening CSR became operational in the mid-2010s, but its real character emerged through iterative redesign. Early on, CSR often behaved like a “comply or explain” system: if you didn’t spend, you explained why in the board report. Over time, policymakers and observers saw the limits of explanation without enforcement. Then came the sharper phase. The Companies (Amendment) Act, 2019 introduced stronger discipline for unspent CSR amounts, including time-bound transfers—an attempt to stop CSR budgets from merely rolling over as an annual excuse. In January 2021, amendments to CSR Rules tightened definitions, formalised implementation norms, and pushed CSR from “best effort” to something that increasingly resembles an auditable process. By 2022, reporting became more structured through Form CSR-2, signalling that CSR would be treated not only as narrative, but also as standardised data. Mandated CSR, in other words, has behaved like a living system—repeatedly corrected by the realities it created. The “who” behind CSR: an ecosystem, not a department CSR is often described as “companies spending money.” In practice, it is an ecosystem. Boards and CSR committees approve policies and budgets; CSR managers negotiate between community need, business expectation, and compliance deadlines; implementing agencies—NGOs, trusts, Section 8 companies—turn budgets into work; auditors check whether the narrative aligns with the books; communities experience CSR not as policy but as a water tap, a classroom, a clinic, a livelihood tool—or as a promise that never arrived. As the rules tightened, the ecosystem became more formal. Compliance expectations for implementing entities hardened, including references to CSR-1 registration mechanisms in the evolving CSR architecture. The uncomfortable geography of CSR: money follows corporate comfort If one wants to understand both the strengths and blind spots of CSR, one must look at maps, not brochures. CSR flows tend to cluster where corporate India clusters. Even within a state, CSR can concentrate heavily in a capital district while multiple districts receive nothing, revealing that CSR funding often follows operational presence and execution comfort more than development need. The preference-for-local-area principle is ethically intuitive—communities living beside industrial sites deserve a share of prosperity. Yet the same preference can reinforce inequality because corporate geography is not human-need geography. The ground reality: why early CSR “worked” and why it still felt thin In the early years, CSR money flowed toward sectors where outcomes were visible and documentation was easier. Education and healthcare dominated. The pattern was almost cinematic in its repetition: a company adopts a government school, repairs classrooms, distributes learning devices, builds toilets, funds scholarships; another company equips clinics, runs health camps, supports mobile medical vans. Then the first twist arrived. CSR became efficient, but sometimes too shallow. NGOs reported a familiar constraint: short-term, tightly restricted funding with limited support for the organisational capacity that sustains impact. CSR often paid for outcomes without paying for the muscle needed to deliver outcomes reliably year after year. The pandemic chapter: CSR discovers the emergency lane When COVID-19 hit, CSR revealed its most valuable trait: speed. Companies pivoted toward healthcare infrastructure, resilience, and digital education, because needs were immediate and undeniable. The boardroom debates changed tone. CSR managers who once argued “education versus environment” began asking “oxygen plant or ICU beds?” NGOs that once wrote proposals for skill training wrote proposals for protective equipment, ration kits, and vaccination awareness. CSR became a rapid-response channel at its best. But the pandemic also made old questions louder: should CSR become a substitute for public expenditure, should corporate funds be routed into central pools or remain close to community delivery, and where does accountability sit when money moves fast? The limitations that forced redesign: why “explain” was not enough A decade into mandated CSR, several persistent constraints stood out across policy discussions, audit observations, NGO experience, and public scrutiny. Unspent funds were too common; some companies treated CSR as a year-end scramble while others delayed due to project risk or weak partner availability. Measurement was thin; reporting often counted rupees and beneficiaries rather than verified outcomes. Geographic concentration stayed stubborn. Implementing ecosystems struggled with documentation burdens, delayed disbursements, and weak access to corporate networks. And CSR sometimes slid into branding—visibility rewarded more than substance. The summary was hard to ignore: CSR mobilised money, but money alone was not impact. The tightening cycle: how CSR became more auditable without killing initiative The redesign logic became clear: keep CSR flexible enough for innovation, but strict enough to prevent negligence and misuse. The 2019 amendment pushed time-bound treatment of unspent funds, often discussed through the lens of an “Unspent CSR Account” mechanism for ongoing projects. The 2021 strengthening of rules moved CSR closer to audit discipline. Penalties for defaults tied to unspent transfers became more explicit. Impact assessment became sharper—especially for large obligations. Reporting, via CSR-2, became more standardised, signalling a shift from “spend and report” to “spend, prove, and learn.” The current scale: big numbers, persistent questions By FY 2023–24, CSR spending had reached very large national scale. Parliamentary disclosures showed CSR expenditure totals rising from ₹27,141.45 crore in FY 2021–22 to ₹34,908.75 crore in FY 2023–24. Education and health remained dominant, while newer categories—culture, animal welfare, environment-linked work, contributions to specified funds—also appeared more visibly. This is the paradox of mandated CSR: it can generate reliable national funding, yet it must continuously fight the gravitational pull toward safe, familiar, easy-to-document interventions. The global mirror: how major democracies handle “CSR” without mandating “2% spend” To compare India with other democratic economies, one must first admit the definitional difference. In many jurisdictions, what India calls CSR spending is split into obligations that look more like risk governance than charity: director duties, modern slavery reporting, non-financial reporting, and supply-chain due diligence. The United Kingdom offers a clear example of responsibility embedded in governance. Under Section 172 of the Companies Act 2006, directors are expected to promote the success of the company while having regard to stakeholders—employees, suppliers, customers, community, and environment. That is not CSR spending; it is responsibility embedded into decision-making. The UK also tightened supply-chain accountability through Section 54 of the Modern Slavery Act 2015, requiring certain organisations to publish an annual statement describing steps taken to prevent modern slavery in operations and supply chains, with the commonly referenced turnover trigger. The strength is clarity and transparency; the weakness is equally obvious—statements can become performative if enforcement and market consequences are weak. Denmark is often cited for making CSR reporting itself mandatory for certain companies through its financial statements framework, effectively turning CSR into an accountability-through-disclosure regime rather than a spending mandate. This early institutionalisation of CSR reporting strengthened transparency, but it still relies on market and civil society pressure to convert reporting into transformation. France took a different route, treating responsibility as prevention. Its 2017 duty of vigilance law requires large companies to publish an annual vigilance plan to identify and prevent serious human rights and environmental impacts across operations and certain business relationships. Compared to India’s CSR, France is not saying “spend 2%.” It is saying “prove you are not causing serious harm—and show your plan.” Germany’s supply-chain approach similarly requires covered companies to maintain risk management systems, preventive and remedial measures, complaint procedures, and reporting focused on human rights and environmental harms. Germany also offers a caution that democracies repeatedly face: once responsibility becomes a compliance machine, debates about burden can trigger exemptions or redesigns. At the European Union level, responsibility is increasingly expressed through two big levers: sustainability reporting, where large and listed companies publish regular reports on social and environmental risks and impacts; and sustainability due diligence, with a directive that entered into force in July 2024 aiming to ensure companies identify and address adverse impacts across operations and value chains. The strength is comparability; the risk is checkbox compliance and the politics of scope and phase-ins. Australia’s Modern Slavery Act 2018 similarly uses a reporting-and-registry logic for entities above a revenue threshold, pushing supply-chain transparency through annual statements. Canada’s supply-chain framework, effective from January 1, 2024, follows the same directional philosophy: increase transparency and encourage responsible practices in relation to forced labour and child labour risks. The United States, by contrast, remains largely voluntary and market-driven on CSR: corporate giving and sustainability reporting exist, but there is no India-style statutory spending mandate at the federal level, and responsibility pressure comes through investor expectation, consumer trust, litigation risk, and sector-specific regulation. What India gets right, what India still struggles with, and what the world can learn India’s unique strength is predictability. Mandated CSR produces a steady flow of social funding that does not rely solely on leadership goodwill or brand strategy. It institutionalises corporate participation in social development. In voluntary CSR environments, philanthropic budgets can shrink sharply in downturns; India’s model is designed to resist that volatility. India’s core weakness is the temptation of “fast spend” over “deep change.” When the KPI feels like “spend by year-end,” there is a structural bias toward interventions that are easy to approve, disburse, and document—often necessary interventions, but not always transformative interventions. The global lesson is that democracies are converging on “responsibility as risk management.” India’s CSR focuses on outward contribution; many other frameworks focus on preventing inward harm and reporting it, especially across supply chains. These approaches are not rivals. They are complements. The direction of travel globally suggests that CSR-style spending alone will not satisfy expectations if core business operations generate social or environmental harm. The next decade: three futures for India’s CSR One future is already visible: CSR becomes more auditable, but not necessarily more impactful. India is moving toward auditable CSR through CSR-2 standardisation, stricter unspent handling, mandatory impact assessment for large obligations, and tighter control on administrative overhead. This increases integrity, but can also turn CSR into paperwork—especially for companies that treat it as a statutory irritant rather than a strategic instrument. A second future is possible and preferable: CSR becomes multi-year and evidence-led, with fewer but deeper programmes, better partner due diligence, stronger district-level diagnosis, and honest outcome measurement. A third future is structural: CSR merges into a broader responsibility regime. As global rules tighten on supply-chain accountability, Indian exporters and global suppliers will face external responsibility expectations regardless of domestic CSR rules. CSR spending may become one pillar of a wider responsible business architecture that includes human-rights diligence, climate transition planning, workforce protections, and governance transparency. Across all futures, the biggest roadblock is capacity: credible implementing agencies, reliable data systems, and internal governance maturity. Without these, CSR and due diligence frameworks can degrade into documents that look impressive and do little. The India CSR checklist If you are a company that crossed any one of the CSR thresholds in the immediately preceding financial year—net worth at or above ₹500 crore, turnover at or above ₹1,000 crore, or net profit at or above ₹5 crore—then CSR compliance is no longer optional. You are expected to compute the CSR obligation as 2% of the average net profits of the preceding three years, approve and follow a CSR policy, ensure spending is on eligible activities under Schedule VII themes, and make the prescribed disclosures in your board/annual reporting. If you are covered, you generally need a CSR Committee. However, you must pay attention to how the law relaxes committee requirements in specific situations. Where an independent director is not required under Section 149, the CSR Committee can be formed without an independent director. If your required CSR spend does not exceed ₹50 lakh in a financial year, the law allows you to skip constituting a CSR Committee; in that case, the Board itself discharges the functions of the CSR Committee. This is not an exemption from CSR—spend discipline, unspent handling, reporting, and compliance expectations still apply. If you implement CSR through an outside agency—an NGO, a trust, or a Section 8 company—you must treat eligibility and registration as non-negotiable compliance hygiene. Many categories of implementing entities are expected to have Income Tax registrations such as 12A and 80G and to be registered through the CSR-1 mechanism, so that the chain of accountability is traceable. If you are spending CSR, remember that CSR is not allowed to become an internal administrative empire. Administrative overheads must remain within the permitted cap and should not exceed 5% of total CSR expenditure for the financial year. If you are a large CSR obligor, impact assessment is no longer a matter of taste. Companies with an average CSR obligation of at least ₹10 crore in the three immediately preceding financial years face mandatory impact assessment expectations for projects above the specified outlay thresholds and with enough time elapsed after completion; the impact report must be placed before the Board and attached to CSR reporting. If you do not spend the full CSR amount in a financial year, you must treat “unspent CSR” as a compliance event, not a footnote. The rule operates on two tracks. If the unspent amount is not linked to an ongoing project, it must be transferred to specified funds under Schedule VII within the prescribed timeline. If it is linked to an ongoing project, it must be transferred to the “Unspent CSR Account” and spent within the permitted window; failing that, it must be transferred as required. Finally, reporting is no longer just narrative. Companies must file CSR disclosures in the prescribed format in board/annual reporting, and CSR-2 has been introduced as a structured reporting mechanism, with timelines governed by the applicable notifications. That is the compliance spine. The strategic question is what separates mature CSR from ritual CSR: whether the company builds multi-year programmes, invests in credible partners, measures outcomes honestly, and resists the temptation to treat CSR as a March transaction rather than a long social contract. ...Read more